Can Dave Ramsey Pick Mutual Funds with 12% Annual Returns?

Skill, luck, or just empty hope?

Dave Ramsey is coming up a lot in my Twitter feed, and it’s a result of two of the topics I primarily follow. The church is one, and Ramsey is a professing evangelical who stands credibly accused of malfeasances not related to his financial dogma. Investing is obviously another, and Ramsey has some (wrong) things to say about it.

Dave, if you’re reading this, please do not start a motor racing team.

Let me start off by addressing one half of Ramsey’s financial punditry, which is the topic of getting out of debt. I acknowledge that the psychological aspect of paying off debt is undervalued. If literally cutting credit cards, eating beans and rice, and paying off the smallest debt first rather than the highest interest rate first is what it takes for you, so be it. Personal finance is personal, but this principle goes both ways. Many members of Ramsey’s target audience could be better served paying off the highest interest rates first and having a nutritious diet that includes an occasional serving of beef or even an avocado.

But in terms of Ramsey’s investing advice, there’s a difference between “what works for you” and just wrong. Once of these points of advice is that investors should ignore fees and pick funds with superior performance. The pitch makes sense on the surface. If a cheap index fund charges 0.03% per year, a more expensive fund charges 1.00% per year, and the more expensive fund outperforms the index fund anyway, you would have been better off in the more expensive fund. That’s easy math, but there are problems under the surface.

One problem is the odds facing the investor in choosing funds that will outperform the index. It is well established that the majority of actively managed funds fail to beat their benchmarks. In 2022, active managers had a relatively good year: only 51% of large-cap U.S. stock funds underperformed the S&P 500. Since 2001, this number has ranged between 45% and 87% and has only dipped below 50% three times.

The numbers are even less rosy for longer periods. Over the last twenty years, just over 92% of U.S. equity funds failed to beat the S&P Composite 1500 index (a broader index than the S&P 500).

But what about the other funds that do outperform the index, the seven or eight percent that beat the S&P 500 or S&P Composite 1500? Even Ramsey isn’t saying that you should pick any old mutual fund. His idea is to pick one that is going to outperform by looking at its previous performance.

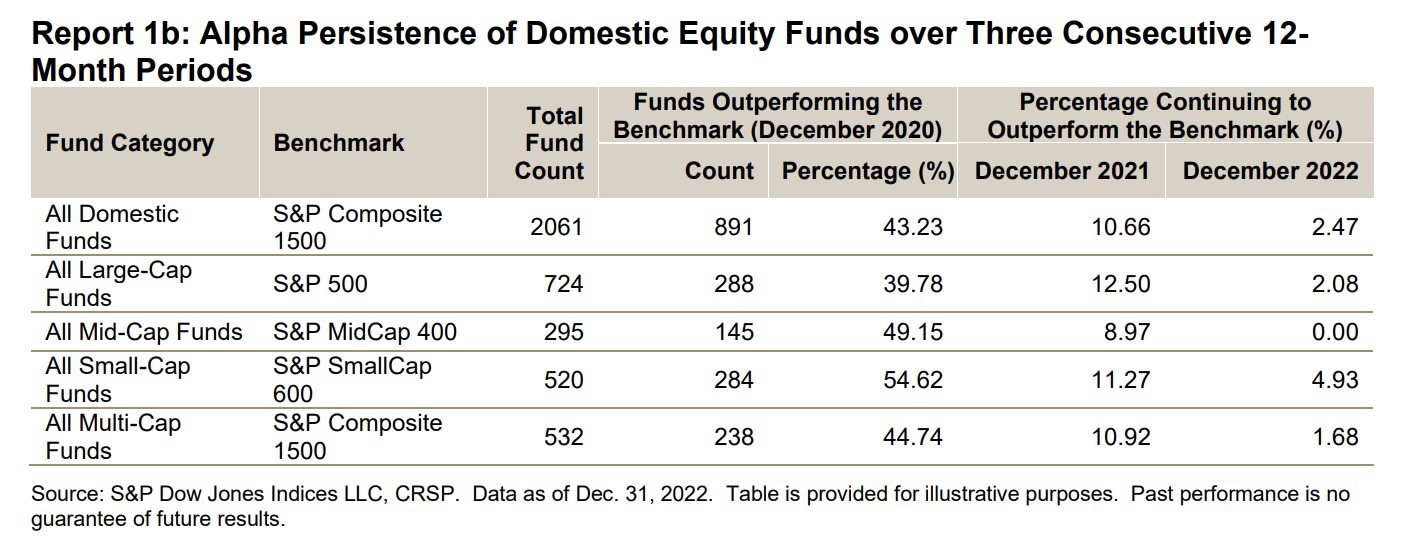

For this, we need to weigh persistence. In other words, do funds that outperform the index continue to outperform the index? The statistics are not in Ramsey’s favor. In 2020, only about 40% of U.S. large-cap funds beat the S&P 500. In the period from 2020 to 2021, the number goes down to 12.5%. In the full 36-month period from 2020 to 2022, only 2.47% of large-cap funds beat the S&P 500.

Over longer periods we see similar results. Of the 178 large-cap funds that were in the top quartile of performance between 2014 and 2018, less than half remained the top quartile after counting one additional year. By the end of 2022, none of these funds remained in the top quartile. Less than 3% of funds that started in the top half of performance between 2014 and 2018 remained in the top half by the end of 2022.

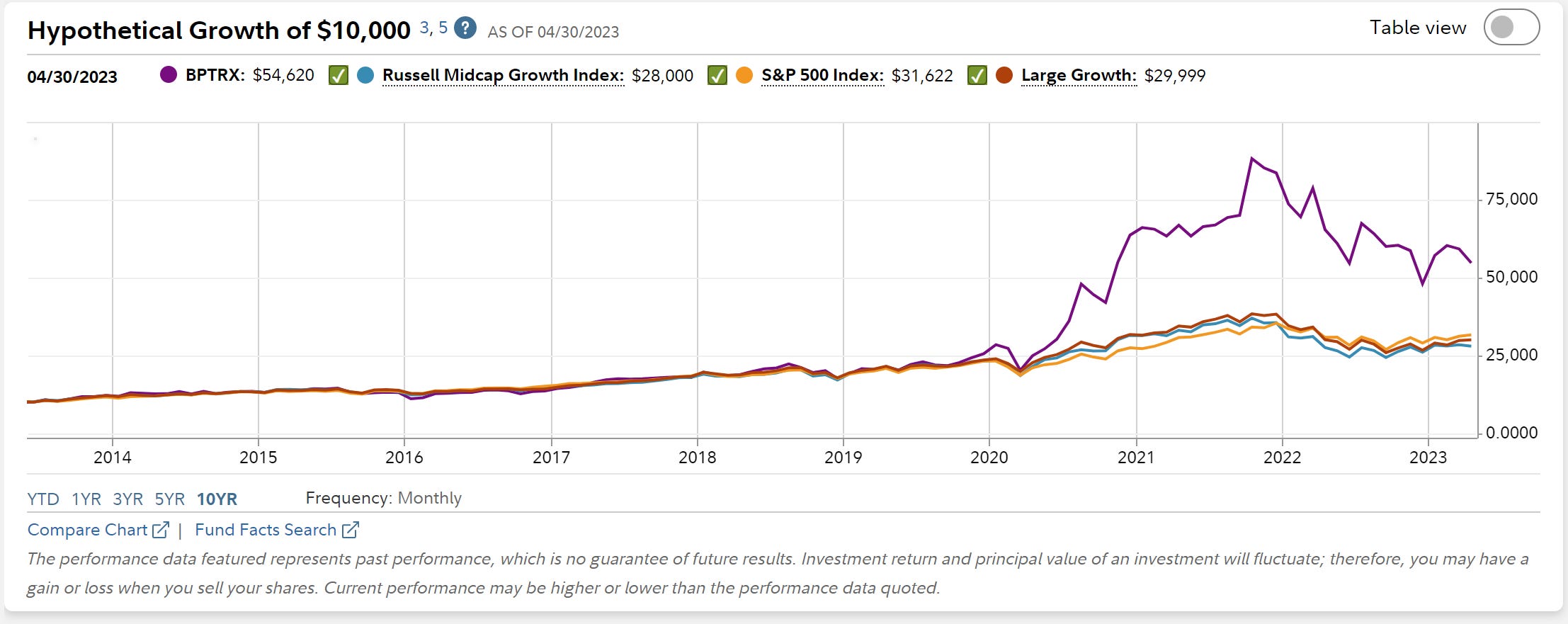

With a little intuition, it’s also easy to see why simply screening off historical performance is an unreliable method: the underlying reason for the outperformance may not be repeated. For example, by using Fidelity’s mutual fund screener, I was able to find that the highest-performing U.S. equity fund (of those listed) over the last ten years was the Baron Partners Fund. The retail shares of this fund (BPTRX) have returned an annualized 18.50% over the last ten years. Since its inception in 2003, its 15.99% annual return has absolutely trounced the 9.88% of Vanguard’s S&P 500 index mutual fund (VFINX) and the iShares ETF equivalent of its Russell Mid Cap Growth index benchmark (IWG). A golf clap for fund managers Ronald Baron and Michael Baron is in order. Nice job.

But an inexperienced fund picker may miss many important details of the fund. As of the end of March 2023, nearly half of the fund is invested in companies run by Elon Musk (Tesla and SpaceX, the latter of which is a private company!). The fund also uses leverage. In other words, it borrows money in order to juice returns (and risk). The fund overall only holds 23 stocks, not enough for a diversified portfolio even if the fund held all of these companies at equal weight.

If I have to guess, I would say that Tesla is a big part of why the fund launched like a rocket in 2020. But if you had identified this trend and bought into the fund in 2021, you would have lost money. And there isn’t an identifiable reason why you should expect outperformance in the future if you buy into the fund now.

Finally, it is impossible from the standpoint of an individual investor to determine whether outperformance like this is the result of skill or luck (or chance if you want to be super-Calvinist about diction). A classic illustration of this is a classroom with 100 students who all flip a coin 100 times to see who can be most consistent in landing heads. We would not suddenly conclude that the “winning” student has superior skill in coin flipping or bet money that he can do it again (we hope). Go ahead and golf clap the Ronald Barons and Peter Lynches of the world. I really mean that. It’s fine. But betting your future on fund managers continuing to outperform is more than likely irrational.

Finally, we need to address this 12% thing in particular.

According to an article from this month on Ramsey’s website, the historical average return of the market from 1928 to 2021 is 11.82%. I don’t know how the unnamed author is getting this calculation. The cited source indicates that $100 invested in 1928 became $761,710.83 by 2021. Therefore, over 94 years (2021 - 1928 +1 = 94), that’s an annualized 9.975% (calculated here). And the Ramsey article conveniently omits a dismal 2022 despite that the article is dated May 11th, 2022. That calculation makes the number 9.636%.

More numbers in this article are suspect. Citing the same source, it states:

That the S&P 500 returned 11.55% from 1990 to 2020. But $29,808.58 (end of 1989) to $592,914.80 over 30 years is 10.48%.

That the S&P 500 returned 12.36% from 1985 to 2015. But $11,823.51 (end of 1984) to $294,115.79 over 30 years is 11.31%.

That the S&P 500 returned 12.71% from 1980 to 2010. But $6,022.89 (end of 1979) to $163,441.94 over 30 years is 11.63%.

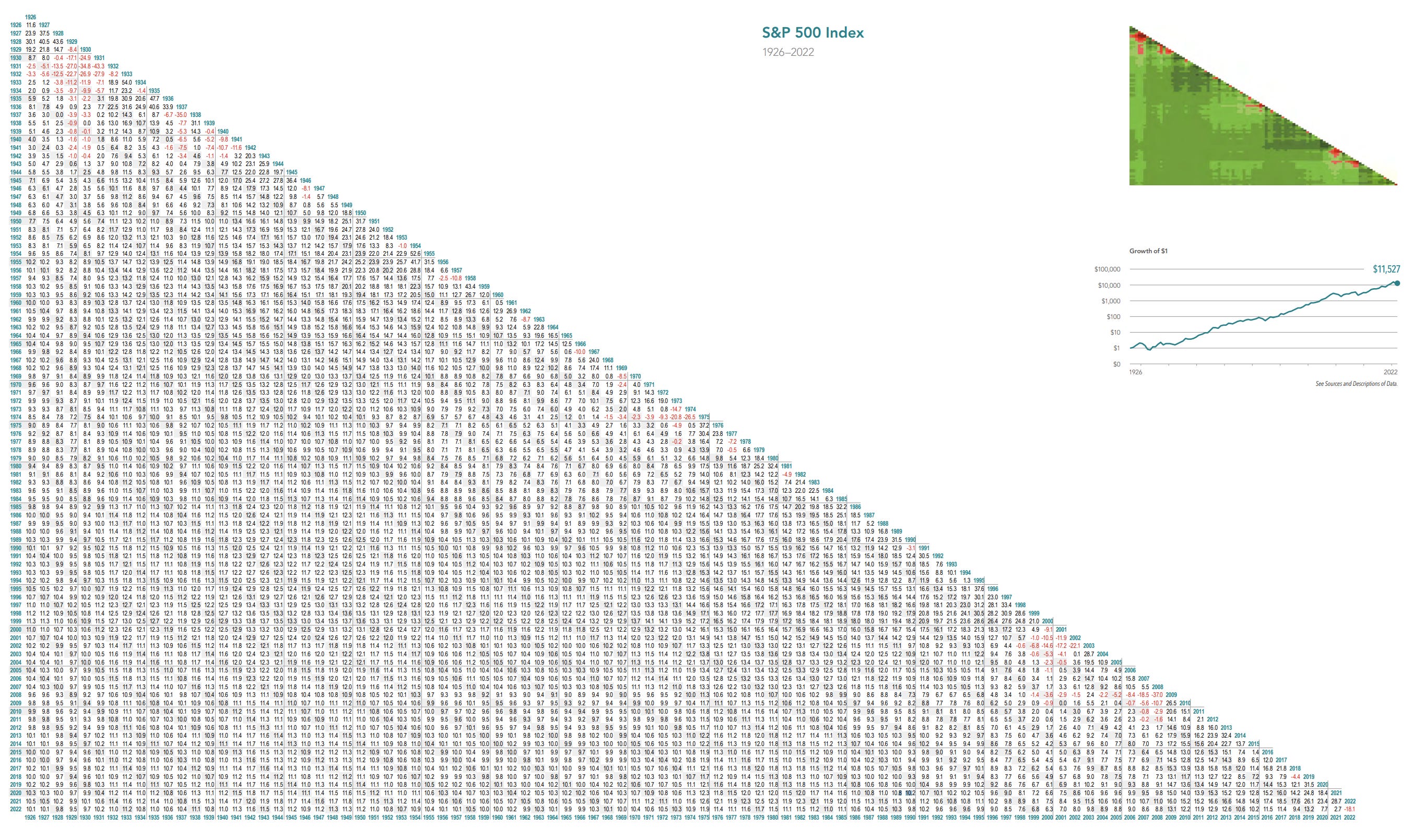

We can find another calculation of historical S&P 500 returns from Dimensional Fund Advisor’s annual Matrix Book, where the historical return of the S&P 500 from 1928 to 2022 is said to be 9.8%. Further annualized calculations of the S&P 500 from DFA are as follows:

from 1926 to 2022 (longest available): 10.1%

from 1990 to 2020: 10.2%

from 1985 to 2015: 11.0%

from 1980 to 2010: 11.4%

We can also go by Vanguard’s S&P 500 index fund to get calculations starting with the fund’s inception in 1976. This is arguably the best measure because it calculates what a real investor could have tangibly achieved.

I simply cannot substantiate Ramsey’s claim that consistent 12% annual returns are possible simply because of the S&P 500’s annual return because the annual return of the index is not consistently 12%.

And even if it were, what was that we said earlier? Past performance is not a guarantee of future results. There is good reason to believe based on valuations relative to company fundamentals that future returns for the S&P 500 may look more like 7%. (That’s another article.) And even if you disagree with 7%, it’s hardly arguable that planning for a 12% return is anywhere near responsible investment advice.

Garrett O'Hara is not a financial professional, just a DIY investing enthusiast. This information is for your information and education only. Particular investments or trading strategies should be evaluated relative to each individual's objectives. Opinions stated constitute my judgment as of the date of when I stated them and are subject to change without notice and are provided in good faith but without responsibility for any errors or omissions contained therein. This information is supplied on the basis and understanding that I and my information sources are not to be under any responsibility of liability whatsoever in respect thereof. Get educated and make your own sound investing decisions.